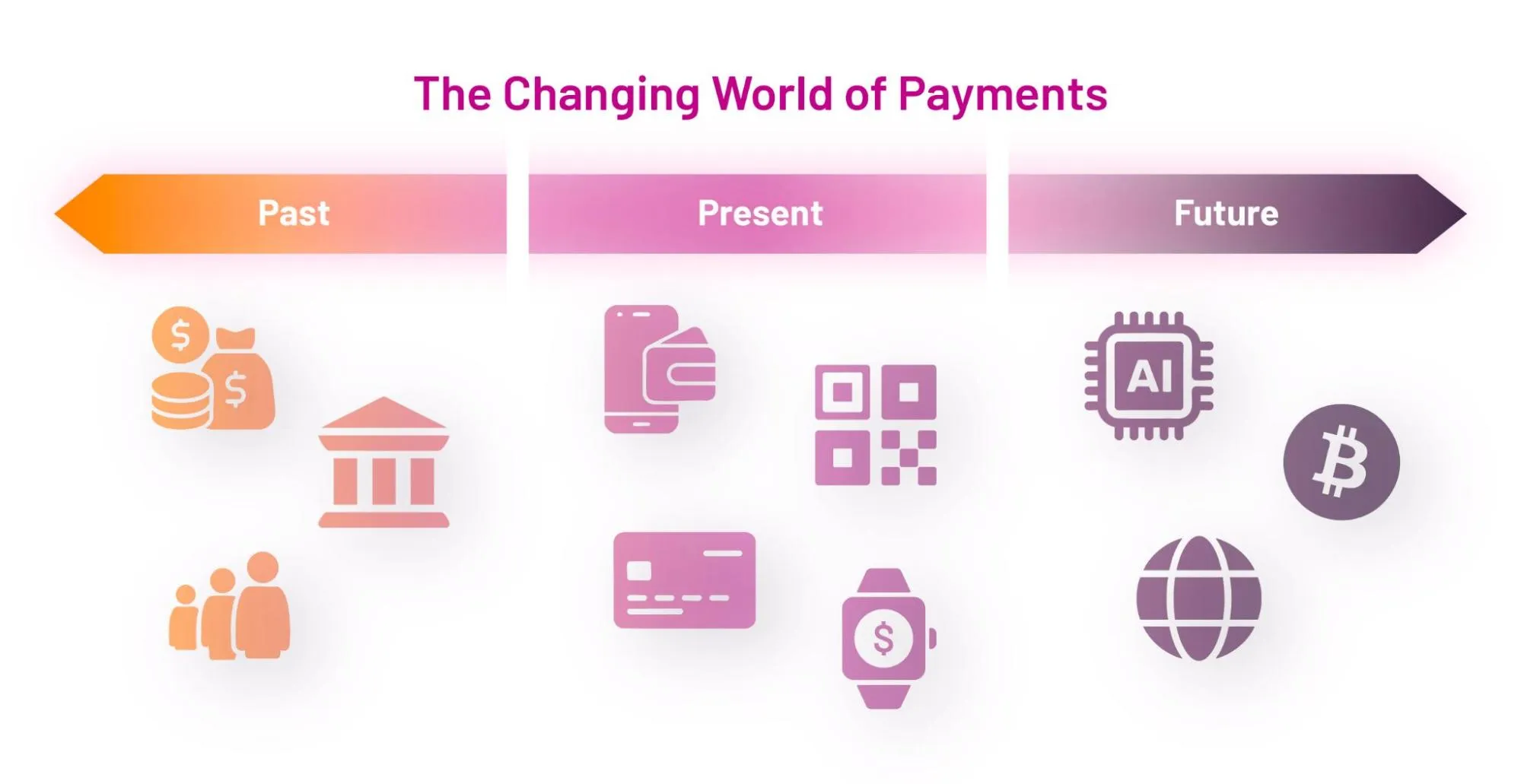

Fig1: Evolution of payments

A Journey We Have All Taken

We have all lived through this incredible evolution of payments. What stands out in this journey is how payments have become quick, easy, and, right now, just a QR scan away. We are yet to witness more. The future promises even faster, smarter, and more invisible modes of payment that will make our payment experience as effortless as a wink.

Indian Digital Payments Landscape

Over the years, India has emerged as a global leader in digital payments, powered by strong public infrastructure built by the government and the Reserve Bank of India (RBI). This foundation has made it possible for everyone - from big corporates to rural shopkeepers to join the digital payments revolution.

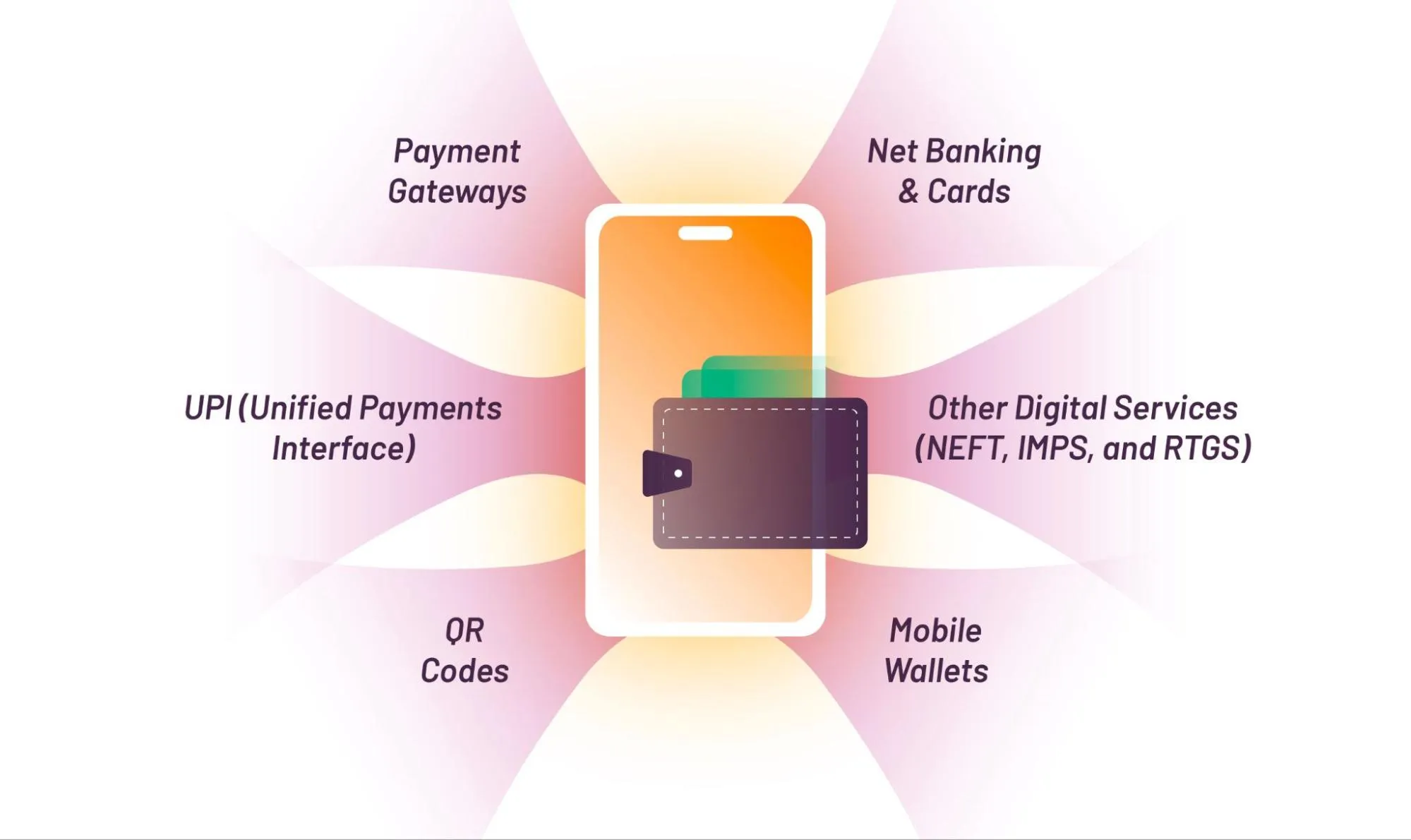

Popular payment solutions in India:

Fig2: Payment solutions in India

- UPI (Unified Payments Interface): Real-time bank transfer platform, powering over 13 billion transactions monthly (NPCI, June 2025), accounting for over 85% of retail digital transactions.

- Mobile Wallets (Paytm, PhonePe, Google Pay, Amazon Pay): Offer contactless payments by storing money digitally on our phones.

- Payment Gateways: Razorpay, PayU, Instamojo, Cashfree, and CCAvenue facilitate online and offline merchant transactions through various payment mechanisms.

- Net Banking & Cards: Credit and debit cards, net banking interfaces are widely used and globally accepted payment types.

- QR Codes: Widely used, especially with UPI and wallets for merchant payments.

- Other Digital Services: NEFT, IMPS, and RTGS for bank transfers, and new platforms like Buy Now Pay Later (BNPL).

This story is not unique to India. Across Asia-Pacific and West Asia, digital wallets, QR codes, open banking platforms, and virtual accounts are driving a similar wave. Countries have developed their own solutions. Examples: GrabPay (Southeast Asia), STCPay (Saudi Arabia), and BenefitPay (Bahrain).

How This Transformation Has Changed Life

The transformation we see in the payment landscape has made daily life simpler for individuals, businesses, and governments:

- Everyday Convenience: Payments anywhere, anytime, and in any format with just a scan or a click.

- Faster Payments: Street vendors, freelancers, and global traders all benefit from increased volumes and instant, low-cost transactions.

- Greater Inclusion and Empowerment: Farmers, migrant workers, and micro-merchants now receive money directly into their accounts, integrating them into the formal economy.

- Easy Government Benefit Transfers: Digital wallets and bank accounts enabled by payment operability have reduced fund leakages, ensuring benefits reach recipients on time.

- Cross-Border Transactions Made Easy: Sending money to family abroad or paying overseas vendors is becoming as simple as a domestic transfer.

- Increased Financial Awareness: Widespread use of digital payment interfaces has fostered consumer confidence and financial literacy.

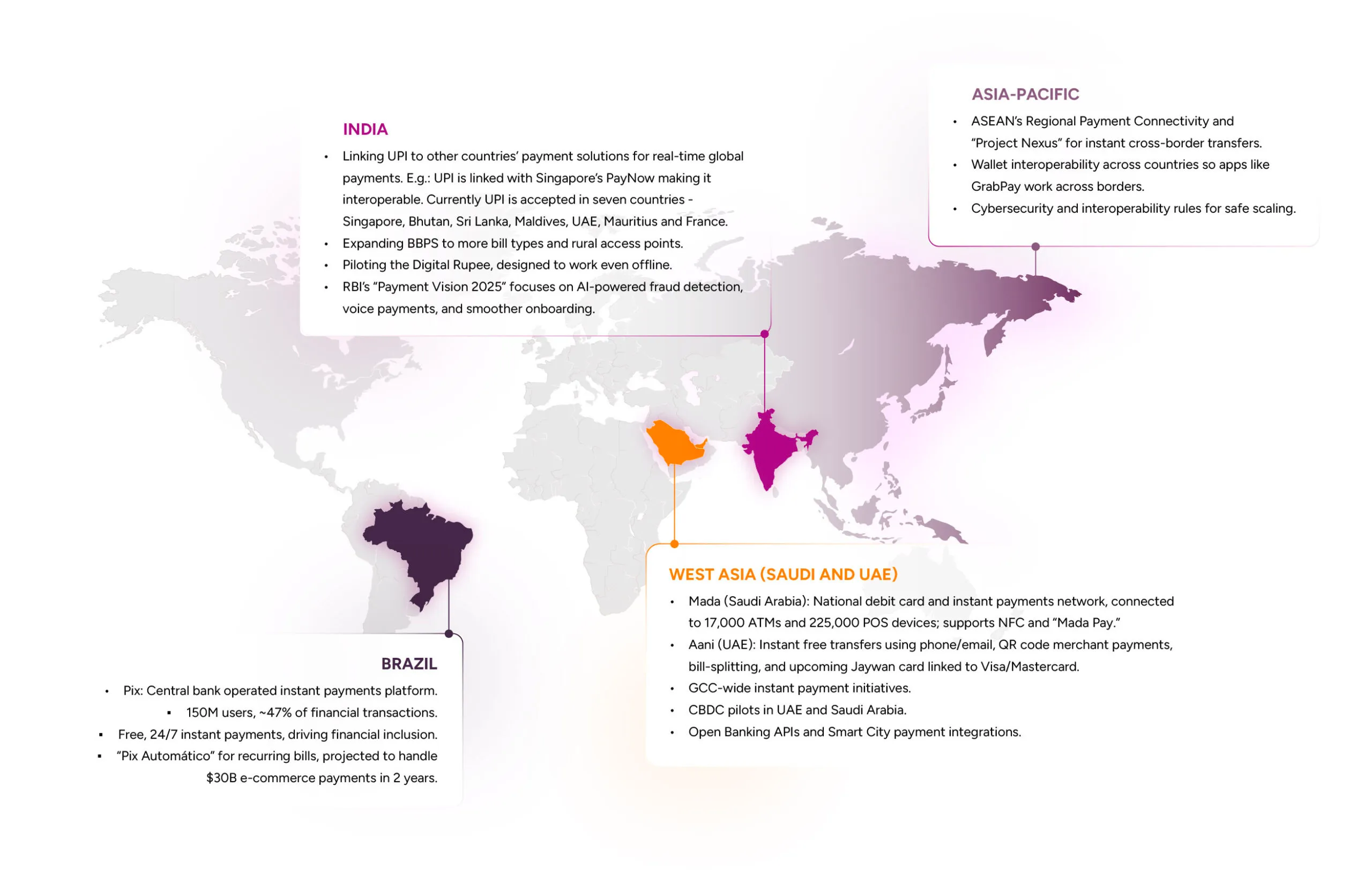

The Infrastructure Powering the Transformation

Payments are no longer just about speed. Around the world, countries are driving innovations in making payments effortless, universal, and accessible to everyone.

Fig3: Transformation of payment solutions in growth markets

Challenges Still Exist

Despite the progress, hurdles remain:

The Future of Payments: From QR Codes to Digital Currencies

Here’s where it gets exciting. Across India, the West Asia, and APAC, the payments space is evolving fast — and the work being done now will make paying for things almost effortless.

Smarter Technology

- AI detecting fraud instantly, reminding about bills, and suggesting the best payment options

- Hyper-personalization: AI-driven products for targeted offers, security, and frictionless payment experiences.

- Voice and wearables payments — saying “Pay my phone bill” to your watch could be as normal as sending a text.

- IoT & New Interfaces: Payments via wearables, cars, smart devices; NFC and UPI Lite for low connectivity zones.

Money Without Borders

- UPI and similar systems link more countries, for instance, low-cost transfers for travellers and businesses. UPI’s framework is evolving into a global standard for instant, low-cost, real-time payments, especially in emerging economies.

- Regional networks like ASEAN’s Project Nexus will make cross-border payments feel like local ones.

Digital Currencies (CBDCs)

- India’s Digital Rupee, UAE’s and Saudi’s CBDCs — these will work online and offline, backed by the government, and could replace cash for many everyday transactions.

Invisible Payments

- Payments are happening automatically in the background for subscriptions, utilities, and services.

Stronger Safety Nets

- Evolving Regulations: Tighter controls on cybersecurity, more robust consumer rights, and a “trust-first” digital ecosystem.

- Tokenization, two-factor authentication, and AI monitoring will make payments safer than ever.

- India has been leading this charge. In May 2025, India introduced the Payments Regulatory Board Regulations, 2025, establishing an expert-led board as the central authority for all payment systems. This ensures more robust, transparent, and accountable oversight.

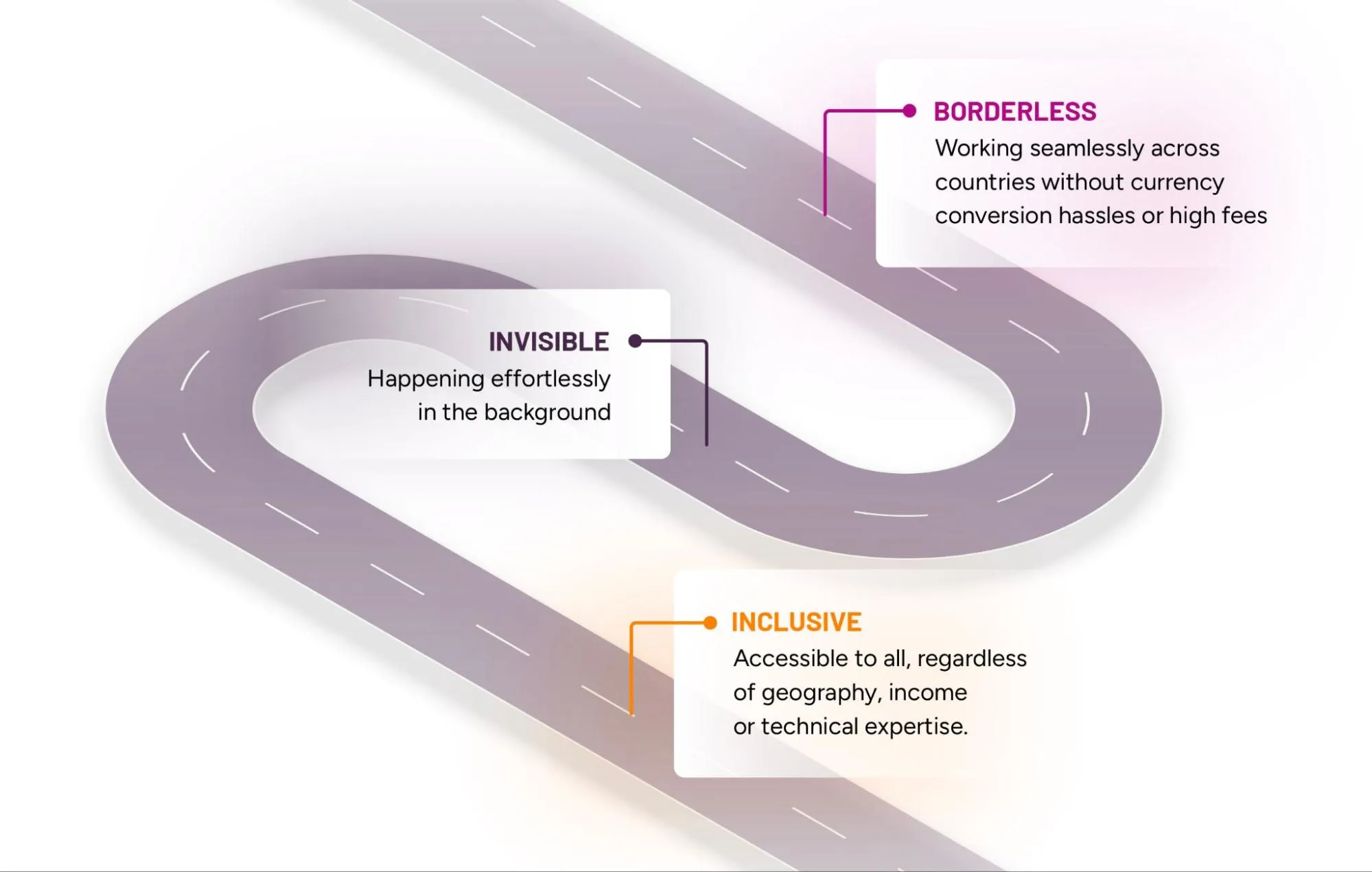

The Road Ahead

We’re heading towards a future where payments are:

Fig 4: Characteristics of future payment solutions

India, the West Asia, and Asia-Pacific aren’t just adapting to new payment trends — they’re defining them. And for billions of people, that means more choice, more speed, and more freedom in how they manage money.