If you take a closer look at the annual report of any leading bank, you are likely to find a reference to a transformation or a greenfield project of their CBS platform. In the early days of delivering digital experience in Banking, IT leaders spent a lot of time on the front-end layer of the platform.This was obvious, given that UI/UX was critical in customer adoption and a type of product stickiness that made them perform transactions from home instead of visiting a branch. However, as the digital landscape grows more competitive and fintechs continue to disrupt the market, banks are realizing the need to address backend limitations that hinder agility and innovation.With the added pressures of today’s macroeconomic environment and persistently low interest rates, banks are shifting their focus to the core of their infrastructure. Fintechs, operating through flexible, cloud-based "banking-as-a-service" models, offer hyper-personalized services at a fraction of the cost due to their lean infrastructure. This shift is pushing traditional banks to rethink their CBS to support real-time customer experiences and drive efficiency.The pandemic further accelerated digital transformation efforts, placing additional strain on the aging CBS infrastructure. Legacy systems, often complex and expensive to maintain, struggle to support the demands of modern applications and hinder fast deployment cycles. To address these challenges, banks are moving towards next-generation CBS architectures that can facilitate seamless, real-time transactions at scale.With this evolution, banks face the challenge of delivering consistent user experiences across a wide range of transaction types—from instant payments (like UPI, NEFT/SWIFT, IMPS) to corporate transactions. Achieving hyper-personalization and real-time responsiveness requires not only rethinking the core banking system but also implementing robust observability solutions. Effective observability across CBS enables banks to gain visibility into transaction flows, proactively identify bottlenecks, and optimize service availability and performance at scale.

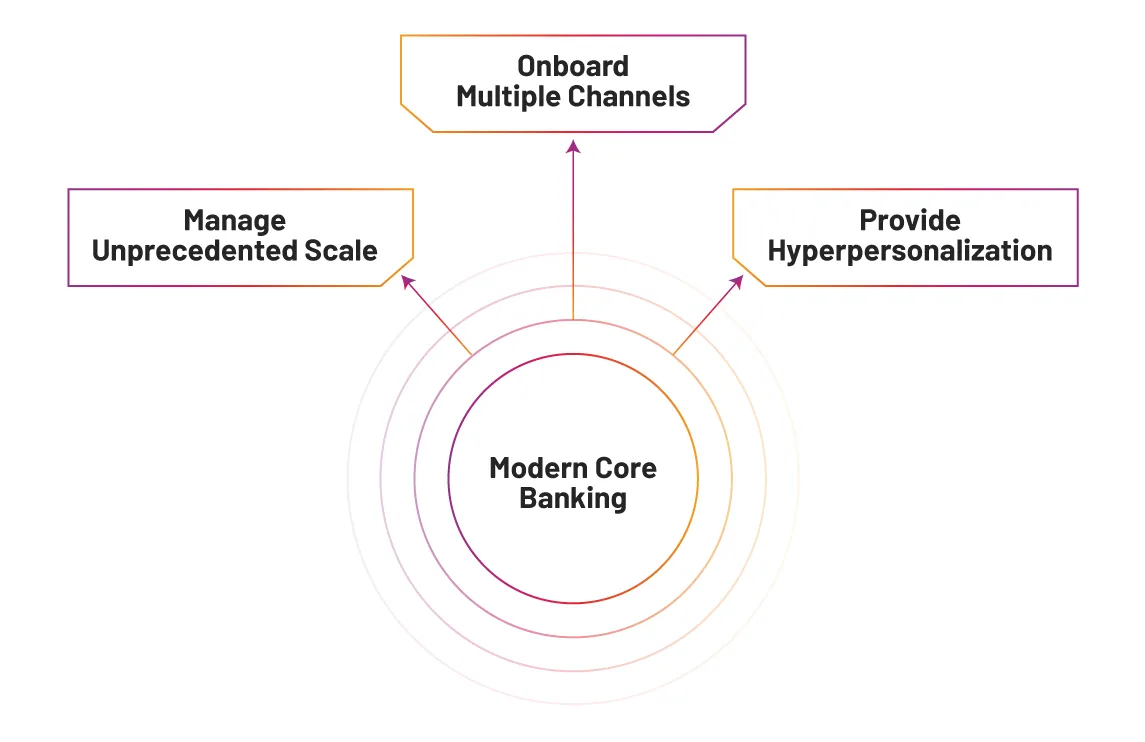

Fig 1: Imperatives for a Modern Core Banking System

The Evolution of Core Banking Systems

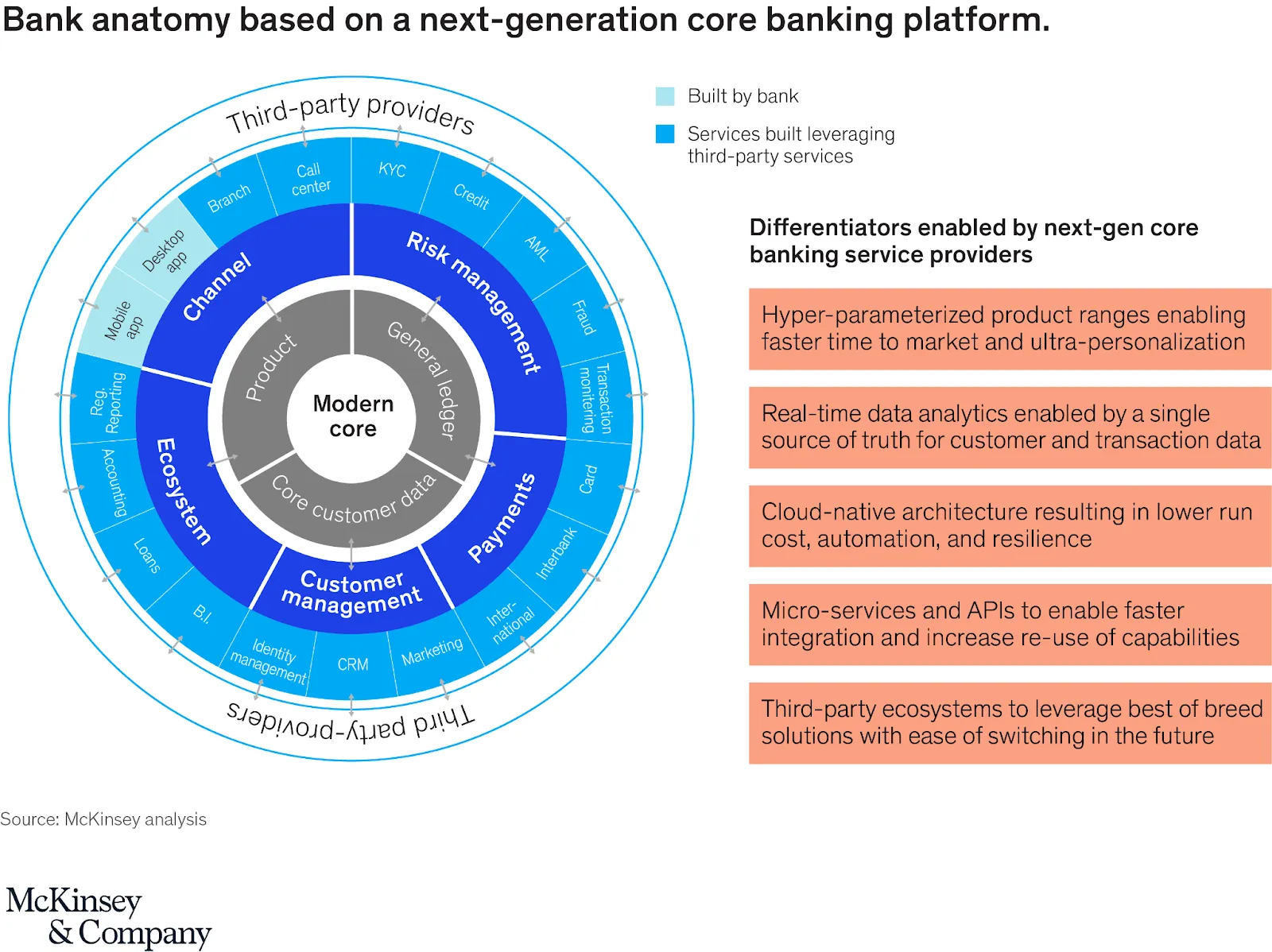

Core Banking Systems (CBS) are the foundational software platforms that handle a bank's primary functions, including processing deposits, loans, payments, and credit operations. Traditionally designed to support basic branch banking, these systems have evolved to accommodate high-volume, real-time transactions driven by the rise of digital and instant payments, such as UPI (Unified Payments Interface) and IMPS (Immediate Payment Service), particularly in markets like India.Today’s CBS must manage the shift from branch-based services to mobile and internet banking, responding to the expectations of a digital-savvy customer base that demands speed, convenience, and reliability.With rapid digitization, CBS platforms are no longer just transaction processing engines; they are becoming enablers of hyper-personalized, multi-service experiences. Modern core banking systems must integrate seamlessly with external services, support real-time transactions, and provide a unified customer experience across various digital channels.Adding to this complexity is the regulatory pressure to ensure the uptime of all critical systems, requiring banks to maintain high success rates and low latencies to deliver a seamless user experience. Regulatory standards also demand continuous compliance, placing a heavy burden on banks to ensure operational resilience and responsiveness in CBS architecture.In response to these pressures, traditional CBS platforms are transitioning to cloud-native, microservices-based architectures that are scalable, configurable, and resilient from day one. By adopting a microservices model, banks can break down their monolithic core systems into modular, independently deployable services, allowing for more flexibility and scalability in response to growing transaction volumes and evolving regulatory requirements. This approach also facilitates collaboration with ecosystem partners, enabling banks to quickly roll out new products and services.

Image Source: McKinsey (Next-generation core banking platforms)

How Banks Are Transitioning to Modern Core Banking Systems

As the demand for scalable, flexible, and cost-effective banking solutions grows, a substantial shift toward modernizing Core Banking Systems (CBS) is underway.The recent McKinsey survey of 37 banking executives revealed that approximately 70% of traditional banks are reevaluating their core infrastructure, with budgets earmarked for upgrades. Over 2020, most banks planned to invest over $10 million, with around 20% committing between $20 to $40 million.This modernization shift is led by firms like Temenos, Mambu, Thought Machine, Finxact, 10x Banking, and Finacle which are pioneering new-age core banking solutions. The global core banking software market is expected to reach $16 billion by 2026, underscoring the momentum of this transformation.Modern core infrastructure provides a foundation for banks to deliver seamless customer experiences, rapidly deploy updates, launch new products, and significantly lower operational costs compared to legacy systems. Banks generally approach this transformation using one of three primary strategies:1. Full Replacement:Some banks choose a complete overhaul of their core system, replacing legacy infrastructure entirely. This approach allows for the adoption of cutting-edge technology but involves significant risk due to complex data migration, the potential for service disruptions, and extended time frames.2. Incremental Modernization:Many banks prefer an incremental approach, integrating new components around their existing legacy systems. By modernizing gradually, banks can manage risk and allow for a phased transition. This method minimizes disruption and provides flexibility in adapting new features over time.3. Greenfield Banking:Some banks establish entirely new digital banks that operate on a modern tech stack. This "greenfield" approach enables banks to test new technologies and services without impacting their existing customer base, allowing for experimentation and innovation in a controlled environment.No matter the strategy, a successful transition to a modern core banking system requires comprehensive observability. Real-time visibility into each layer—from transactional flows to backend operations—ensures that the modernization journey is smooth, reduces risks of service disruption, and supports the seamless, efficient transformation that banks aim to achieve.

Observability in Modern Core Banking Systems (CBS): A Detailed Approach

As Core Banking Systems evolve, encompassing legacy platforms, transitioning systems, and cloud-native architectures, the observability strategy must accommodate this diverse landscape. Core Banking Systems typically function as a combination of branch flows, channel flows, and API flows, interfacing with upstream channels (like mobile apps, and ATMs) and downstream processing engines, databases, and middleware.Legacy CBS systems often utilize C/C++, while modern architectures are built with Go/Java on cloud-native, Kubernetes (K8s)-enabled platforms. Given this setup, comprehensive observability is essential for tracking the end-to-end flow of transactions across diverse channels and touchpoints.Here’s how observability should be approached for a CBS, capturing key metrics and establishing a detailed view of transaction health, performance, and system stability.

Key Elements for Core Banking Observability

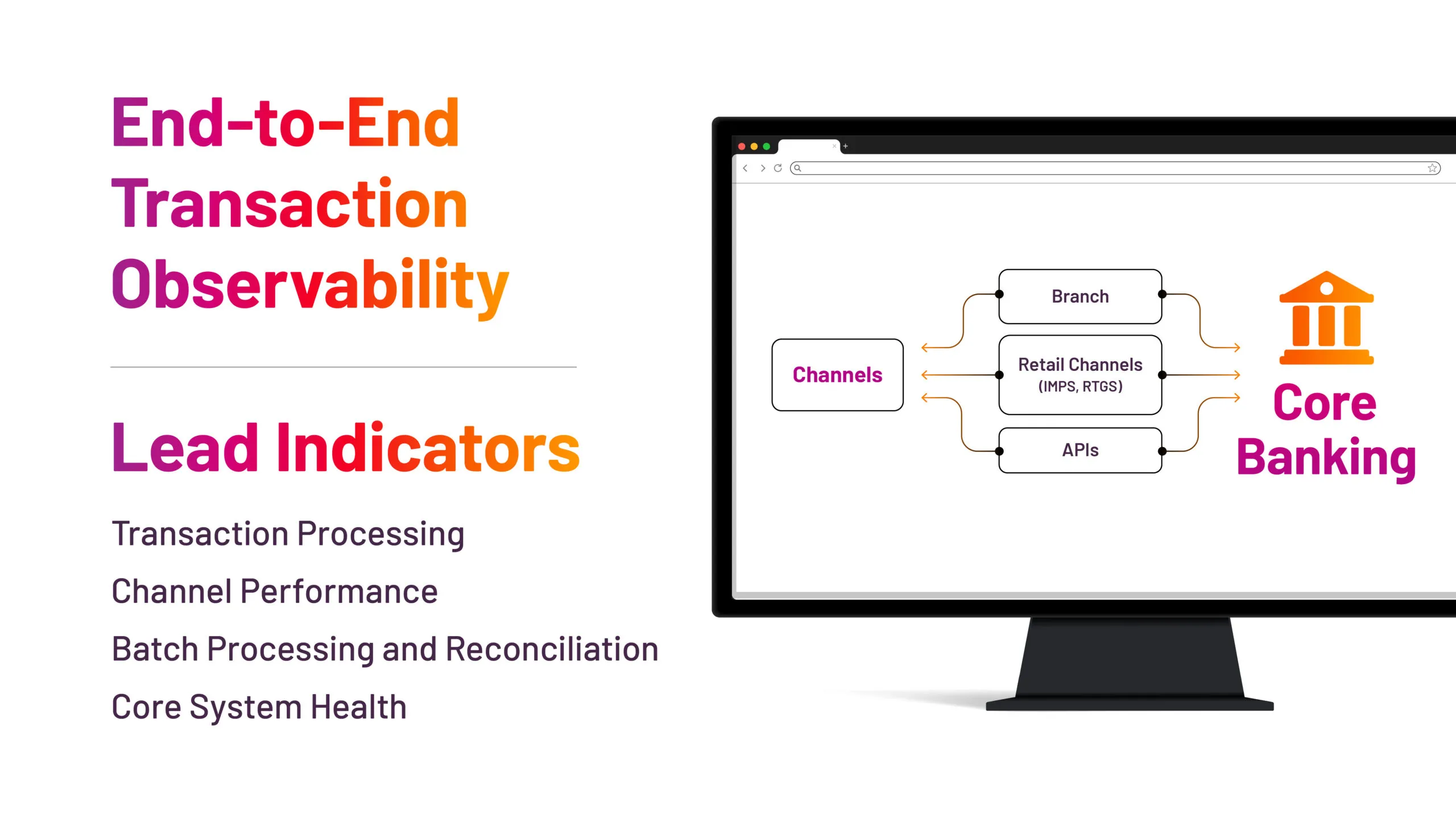

1. End-to-End Transaction Observability:

- Channel and Upstream Traffic Correlation: It’s crucial to monitor upstream traffic from various channels (ATM, mobile, POS, instant payments) and correlate it with CBS traffic to detect transaction drop-offs and identify bottlenecks.

- CBS Traffic Monitoring: This includes measuring lead indicators such as transaction throughput, latency, response/error codes, and particularly asynchronous latencies, which are common in CBS environments.

2. Lead Indicators for Monitoring Modern CBS with Business Journey Observability:• Transaction Processing Indicators:

- Transaction Success Rate: Track the percentage of successful transactions versus total attempts across channels (e.g., mobile, web, ATM). Examples include monitoring success rates for specific services like fund transfers, loan disbursements, and bill payments.

- Transaction Latency: Measure the end-to-end time to process transactions, with a focus on high-value transactions (wire transfers, loan applications). Breaking this down into specific steps like authentication, approval, and settlement provides deeper insights.

- Failure Rate by Transaction Type: Monitor failure counts segmented by transaction types (e.g., ATM withdrawals, card payments), along with failure reasons (e.g., technical errors, insufficient funds).

• Channel Performance and Availability Indicators:

- Channel Uptime: Track uptime for critical channels (e.g., mobile banking, ATMs, branch networks) to ensure uninterrupted service. Downtime impacts customer experience and transaction volume.

- API Response Time: Measure real-time API latency for digital channels interacting with CBS. This impacts transaction speed and user experience.

- Service Availability: Monitor the availability of key services such as account inquiries, fund transfers, and loan processing to prevent service disruptions.

- User Authentication Success Rate: Ensure smooth authentication flows, especially with multi-factor and biometric verifications, as they are critical for both security and transaction success.

- Network Response Time: Track the time taken for requests from different channels to reach the CBS. Any latency here can indicate network bottlenecks or connectivity issues.

• Batch Processing and Reconciliation Indicators:

- End-of-Day (EOD) Batch Processing Time: Monitor EOD processing times for settlement of transactions, essential for accurate reporting and reconciliation.

- Reconciliation Success Rate: Track the percentage of successfully reconciled transactions, ensuring there are no mismatches with card networks (Visa, Mastercard) or third-party processors.

- Settlement Latency: Monitor how long it takes for transactions to move from pending to settled, especially important for high-value payments like wire transfers.

• Core System Health Monitoring:

- Database Performance: Monitor CBS database performance (e.g., Oracle, SQL Server) to identify connection issues, slow queries, and capacity constraints.

- CPU and Memory Utilization: Ensure server resources are not overloaded, tracking CPU and memory metrics to maintain optimal performance.

- Storage and Backup Health: Regularly check transaction storage and backup systems for reliability. Issues here could risk data integrity and long-term reliability.

Figure 2: Key Elements of CBS Observability

Additional Considerations: Addressing Asynchronous Transactions and Custom Data Collection

One of the main challenges in achieving effective observability in Core Banking Systems (CBS) is the prevalence of asynchronous transactions. Traditional Application Performance Monitoring (APM) tools primarily target synchronous function calls and often fall short in capturing the complete transaction flow that CBS demands. Observability in CBS must extend beyond conventional APM to account for the following aspects:1. Trace and Transaction ID Correlation:Since CBS transactions often span numerous touchpoints and services, transaction IDs need to be traced across logs, metrics, and traces to map the entire journey. This involves adding transaction IDs in trace logs and utilizing payload data to provide context, allowing for the stitching of IDs across different system layers. This approach enhances the ability to monitor a transaction’s progress and pinpoint potential issues across all points of interaction.2. Business Journey Observability:Rather than focusing on isolated service monitoring, Business Journey Observability connects the dots across the full process. For instance, monitoring a UPI payment from initiation through settlement involves multiple layers, each producing unique telemetry. By consolidating these layers into a single journey map, banks gain comprehensive coverage and deeper root cause analysis capabilities. This end-to-end view is essential for understanding user experience and operational efficiency in real time.3. Custom Data Collection and Adapters:Core Banking Systems often need customized adapters to gather data from multiple database sources. These adapters enable the collection and aggregation of transaction metrics, such as the number of users or volume of IMPS/SWIFT transactions, across various services. Stitching this information across different transactions is critical for creating accurate, insightful transaction metrics that inform business and operational decisions.Together, these strategies enable CBS observability to meet the demands of modern digital banking, providing visibility across asynchronous processes, correlating transaction details across layers, and ensuring comprehensive monitoring.

Scale and Reliability in Core Banking Systems (CBS)

CBS platforms serve institutions of varying sizes, from smaller banks handling around 10 million transactions daily to larger banks processing up to 80 million. This scale places immense pressure on core services, and any disruption can lead to severe downtime and customer dissatisfaction. Consequently, seamless monitoring is essential to ensure service reliability and to preemptively identify potential disruptions before they impact customer experience.

Challenges with Traditional APM Tools

The backend of many core banking systems typically operates on compiled languages like C/C++, which presents unique challenges for instrumentation. Traditional Application Performance Monitoring (APM) tools, such as Dynatrace or AppDynamics, are optimized for environments running interpreted languages like Java or Python. This makes it difficult to capture critical insights in compiled environments, potentially missing essential performance metrics and system health indicators.

Moreover, many traditional APM tools still depend on instrumentation to gather traces, which can often interfere with internal services and cause conflicts, leading to service outages. Instead of preventing downtime, these intrusive methods can trigger it.

Given this constraint, banks require a more tailored observability approach to capture real-time, end-to-end visibility into every layer of their CBS infrastructure.

Domain-centric observability with Logs, Metrics, and Traces

At VuNet, we specialize in delivering comprehensive, end-to-end monitoring of Core Banking Systems (CBS), spanning from the Web Layer to Middleware Applications to the Database Layer. Using a domain-centric first approach, our observability platform combines the following capabilities:1. Comprehensive Telemetry Collection

- Logs, Metrics, and Traces: Our platform brings together logs, metrics, and traces across CBS components, covering application telemetry for Java/microservices, Oracle WebLogic, IBM WebSphere, and more.

- Semantic understanding with Low-Code Adapters: We offer pre-built and low-code adapters tailored for various CBS functions, capturing response codes, error codes, and process (proc) codes with a semantic dictionary for a holistic view of application and transaction performance.

2. Transaction-level and Aggregated Visibility

- Turnaround Times at Touchpoints: By analyzing logs and metrics, we provide both transaction-level insights and aggregate views of turnaround times at every touchpoint in the transaction flow, from customer initiation to backend processing.

- Process Code Monitoring: Our deep understanding of application and process codes (proc codes) helps identify transaction stages, shedding light on where and why transactions might face issues. This visibility is essential for fast troubleshooting, and minimizing downtime.

3. Specialized Monitoring and Domain-Centric Configurations

- Key Operational Metrics: The platform is extensible for banking domain, allowing insights into specific metrics such as the number of active users, pending SWIFT and RTGS transactions, and session statuses. This provides targeted visibility into essential banking operations.

- Core Service Monitoring: Extending observability to critical CBS services, we capture connection-level statistics like TCP connections and monitor metrics such as time wait increments. By examining performance at the port level, we ensure that core services operate efficiently, preventing bottlenecks and performance degradation.

By focusing on these targeted observability layers, VuNet’s domain-centric platform enables deeper monitoring, faster root cause analysis, and a robust understanding of the critical metrics needed to keep software for Core Banking Systems performing optimally.

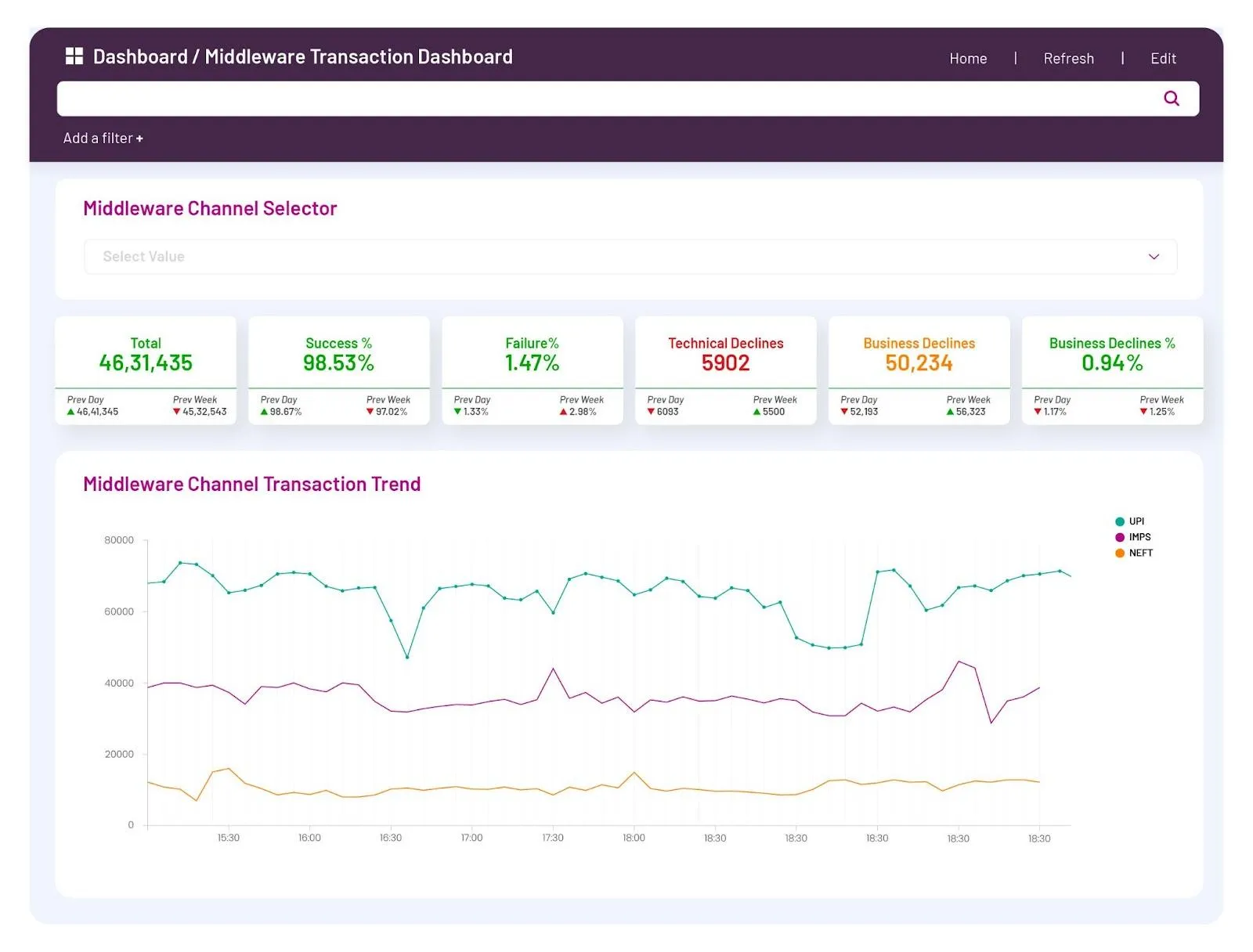

Figure 3: Snapshot of a channel view with its slice and dice across Transactions, TATs, success rates etc.

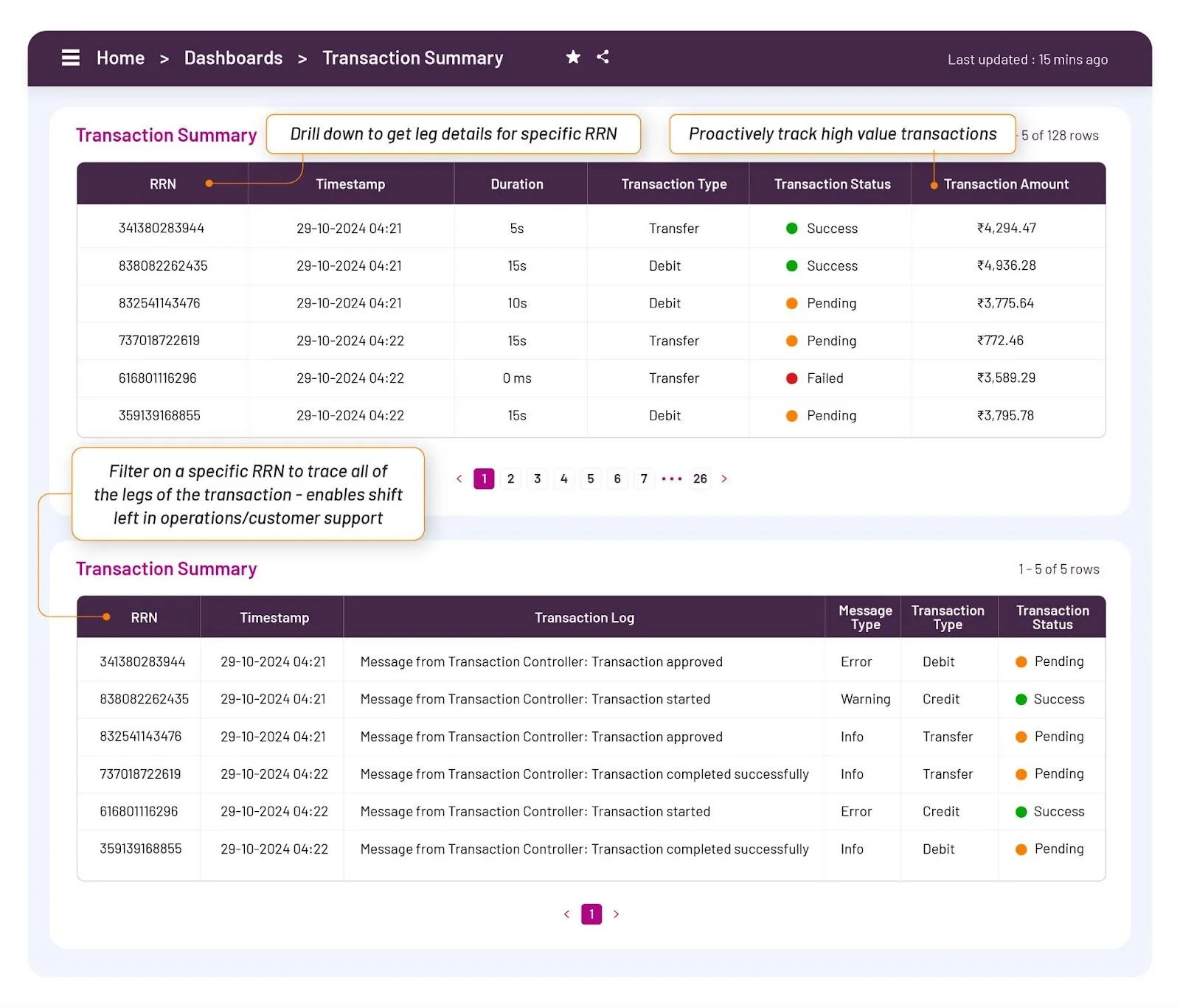

Figure 4: Transaction Summary Dashboard for Customer Support with Real-time Insights

Real-World Impact: How VuNet’s Observability Adds Value

VuNet’s observability platform is integral to the core banking operations of a major private bank spanning multiple geographies. It efficiently handles over 5,000 transactions per second (TPS) for CBS ensuring stability and responsiveness across the bank's digital infrastructure.Our platform supports multiple teams across IT operations (L1, L2, SRE) and business operations teams who rely on real-time monitoring and advanced troubleshooting to maintain smooth operations. Business operations teams utilize the platform daily to monitor critical financial workflows in branch and channels (including UPI, IMPS, and corporate payments) with real-time insights that expedite issue resolution and enable data-driven decision-making.

Benefits of Comprehensive Observability for CBS

Comprehensive observability provides in-depth visibility into CBS’ performance, which supports various key personas within the bank:1. IT Operations & SRE Teams: Real-time alerts and telemetry across infrastructure layers enhance incident management, significantly reducing Mean Time to Detect (MTTD) and Mean Time to Resolve (MTTR) for critical issues. This capability helps teams address issues before they impact end users.2. Business & Application Owners: With real-time visibility into transaction success rates, user experience, and channel performance, business and app owners can make informed decisions that improve service delivery, optimizing channels for a seamless customer experience.3. Compliance & Regulatory Teams: The platform enables monitoring for regulatory compliance by tracking uptime, success rates, and other vital metrics, supporting adherence to industry standards and maintaining operational resilience.

Figure 5: Real-World Benefits of CBS Observability4. Cost Efficiency and Value: The observability insights from VuNet have helped the bank drive operational efficiencies, saving $12.5 million annually. These savings arise from minimized downtime, reduced incident frequency, and enhanced monitoring that improves resource utilization. Through real-time insights and optimized workflows, VuNet’s observability platform not only ensures high performance but also delivers a compelling return on investment by reducing the Total Cost of Ownership (TCO) associated with CBS operations.

Conclusion: Elevating Core Banking with Strategic Observability

As banks transition to next-generation core banking systems, observability for core banking is not just an operational requirement but a strategic imperative.By partnering with leading banks, VuNet Systems is embedding observability as a core pillar of their digital transformation, providing real-time insights that ensure seamless migrations, optimized system performance, and minimal disruption to services.Observability empowers teams across the organization—IT, business operations, and customer support—enabling them to quickly identify and resolve issues, monitor transaction flows, and provide proactive customer nudges in case of failed transactions. This proactive approach aligns directly with banks' goals for hyper-personalization, allowing them to tailor services and support based on real-time transaction data.In a landscape where financial services are evolving rapidly, robust observability for Core Banking Systems delivers more than operational efficiencies; it creates a foundation for resilience, innovation, and customer-centric banking. As the industry continues to shift towards cloud-native, API-driven architectures, observability will remain essential, enabling banks to stay competitive, compliant, and ready for the future of banking.