Setting the Context: The New Digital Battlefield for NBFCs

Over the last few years, Non-Banking Financial Companies (NBFCs) have transformed dramatically. Traditional lending models have shifted towards digital-first operations—loan origination, customer applications, eKYC verifications, credit underwriting, disbursements, repayment scheduling and customer servicing are now mostly online. Today, NBFCs are defined and judged not just by their lending portfolios or competitive interest rates, but by how quickly loans are approved, how smoothly transactions are processed, and how reliably disruptions are managed. However, the systems powering these journeys are complex, involving hundreds of interconnected applications, databases, and third-party integrations like credit bureaus and payment gateways. Ensuring that each customer transaction is seamless requires more than traditional monitoring. It requires deep, real-time business observability - a unified view that connects IT performance with customer journeys and business KPIs.

Challenges NBFCs Face with Digital Transactions

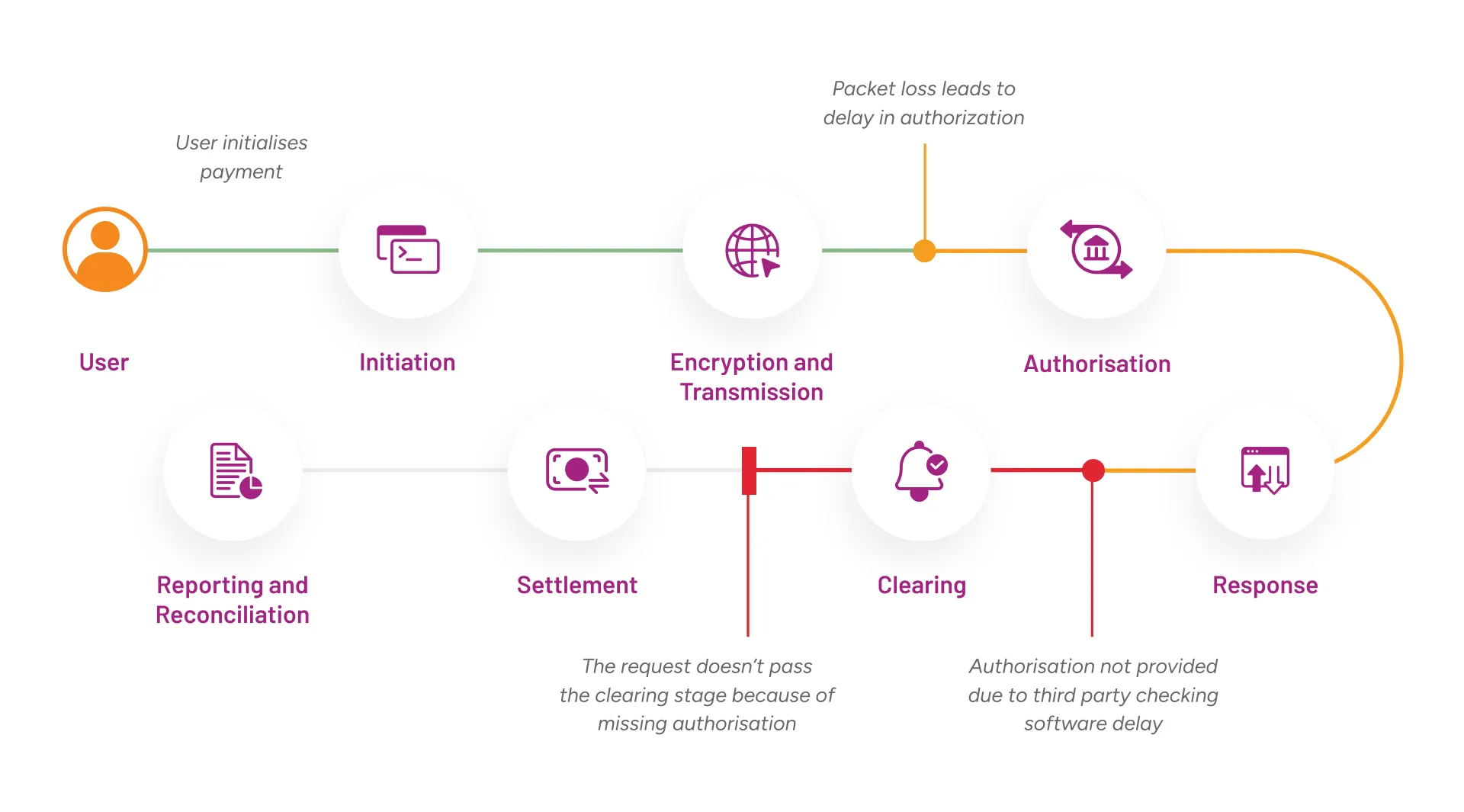

Fig 1: Sample Challenges in a User Payment Journey

As digital transactions surge, NBFCs grapple with distinct operational challenges:

- Transaction Failures Across Channels: EMI payments, loan disbursements, and auto-debits can fail due to third-party gateway issues, network latencies, or backend bottlenecks.

- Manual Delays in Lending Workflows: Lending workflows often involve multiple approval stages, systems, and manual interventions, creating hidden latencies that increase turnaround time (TAT).

- Customer Drop-offs During eKYC or eMandate: Customer onboarding consumes 80-90% of operational bandwidth, making it a critical and lengthy process. Delays during OTP verification, Aadhaar XML fetching, or PAN validation can result in users abandoning applications mid-way.

- Third-Party Dependencies Risks: Integration with external systems like CIBIL, NSDL, UIDAI, and bank APIs adds multiple points of failure, directly impacting approval rates and processing times.

- Data Layer Bottlenecks: Heavy loads on databases during month-ends or peak periods can lead to deadlocks, slow queries, and transaction timeouts.

- Lack of Unified Visibility: Teams struggle to pinpoint exactly where in the journey a transaction failed or performance degraded.

PwC’s 2023 report shows that digital lending makes up over 10% of total NBFC disbursements and is projected to double by 2027. That means ensuring every digital journey runs smoothly is no longer optional—it’s critical to business continuity and growth.

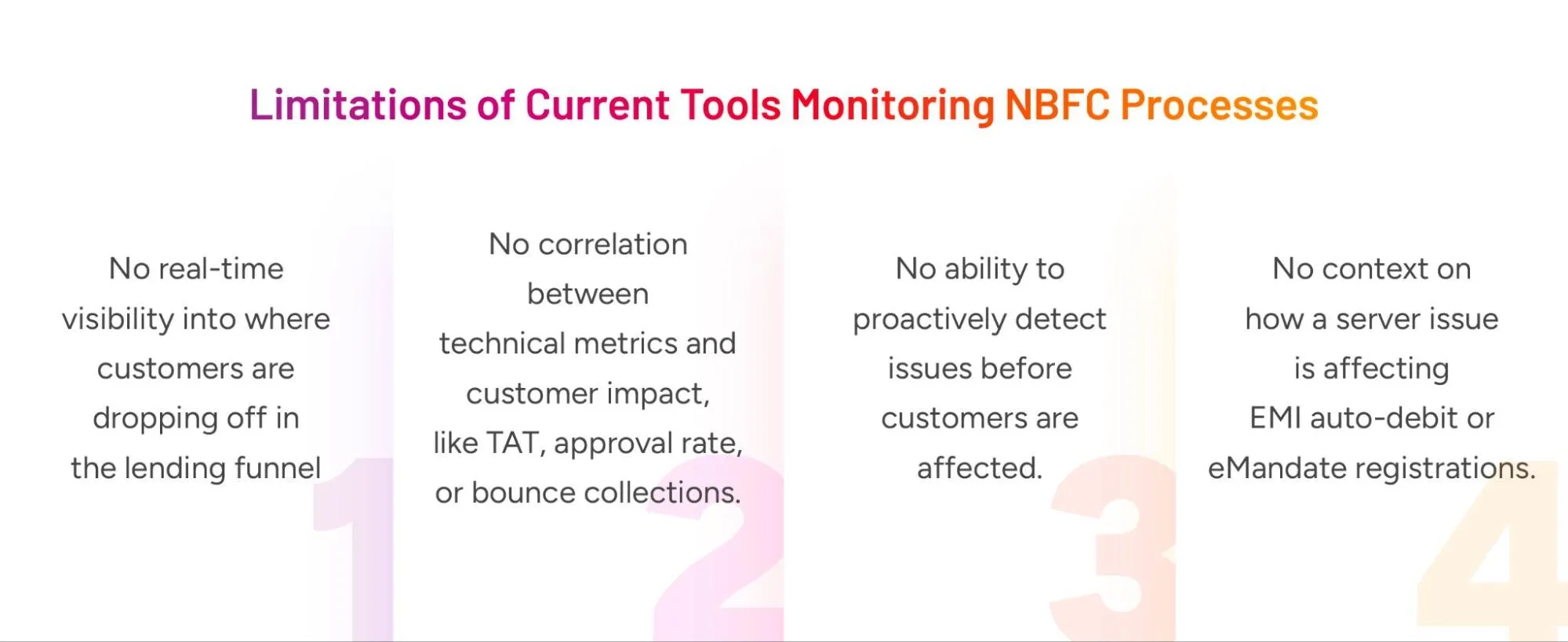

The Limitations of Current Tools

Traditional monitoring setups simply can’t keep pace with this complexity. Most NBFCs still rely on:

- Infrastructure Dashboards: CPU utilization, memory, and uptime statistics.

- Application Logs: Static logs collected after the fact.

- Isolated Alerts: Threshold-based triggers on isolated metrics with no business context.

- Manual Correlation: Teams manually piece together data from different systems to troubleshoot

What they miss:

Fig 2: Limitations of Current Tools Monitoring NBFC processes

In essence, current tools tell you something is wrong, but not what, why, or how it impacts the business, in many cases causing direct revenue loss.

The Need for Business Observability

Given the stakes, NBFCs need to move beyond uptime metrics to business-centric observability. Business Observability bridges the gap between infrastructure health and business success by:

- Tracking business journeys end-to-end (e.g., from lead capture, eKYC, underwriting, to disbursal and repayment).

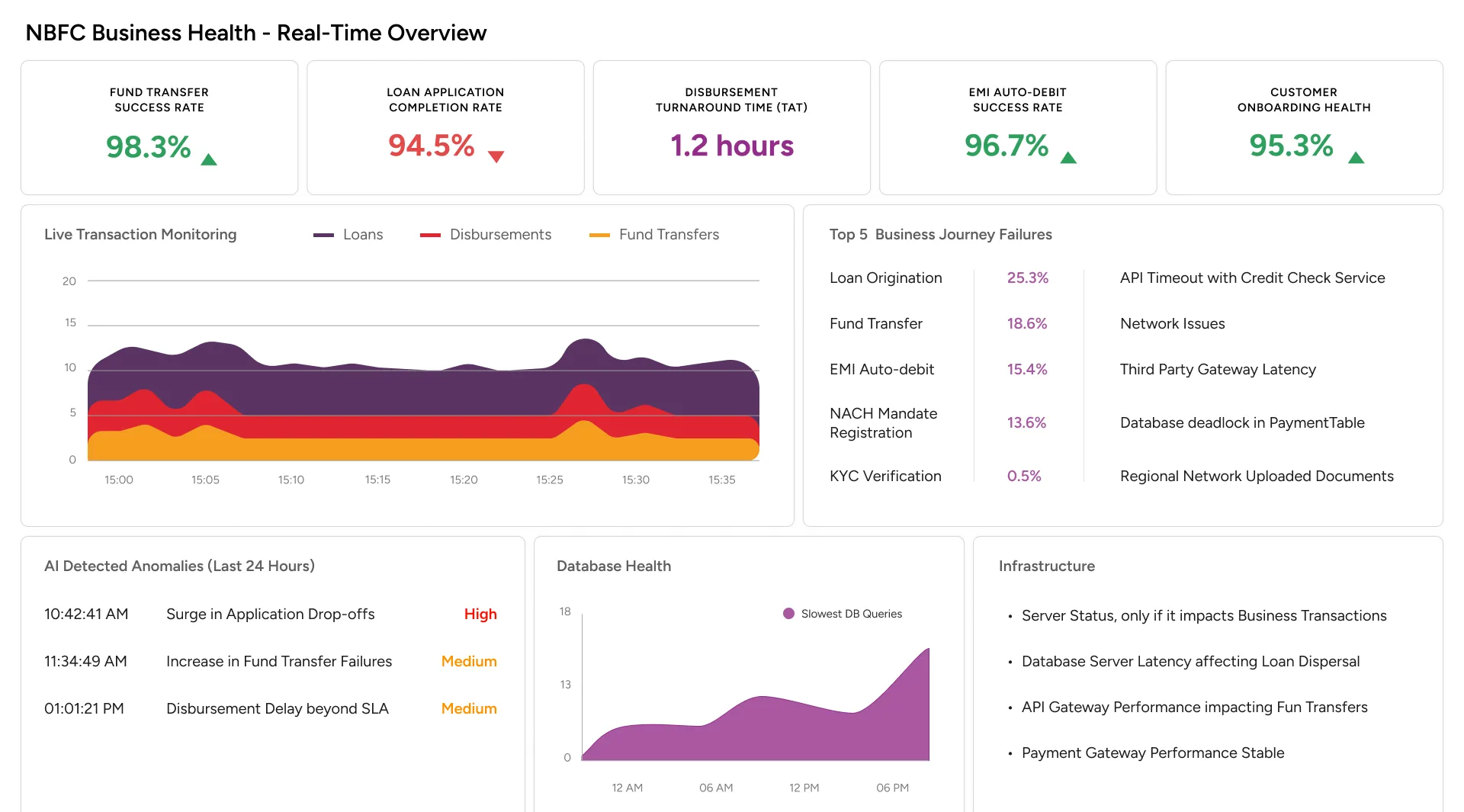

- Connect technical issues with business KPIs (e.g., loan application completion rate, disbursement TAT, EMI auto-debit success rate, etc.)

- Correlating application, infrastructure, and transaction data on a single canvas for 360° visibility.

- Enabling real-time, actionable insights—not just technical metrics, enabling actions prior to customer or revenue impact.

With business observability, NBFCs can move from reacting to outages to proactively safeguarding customer experiences.

How VuNet Powers Business Observability for NBFCs

VuNet’s Business Observability Platform is purpose-built for complex, transaction-heavy businesses such as BFSI. It empowers NBFCs with real-time insights across the digital lending lifecycle, enabling a proactive stance in ensuring seamless customer experiences.

- Visualize Complete Business Journeys Track each critical step, including the many manual workflows involved in the lending process, by mapping it into VuNet’s platform.

E.g.: Lead Capture → Application Submission → eKYC → Credit Check → Risk Scoring → Approvals and Sanctions → Disbursal → Repayment.

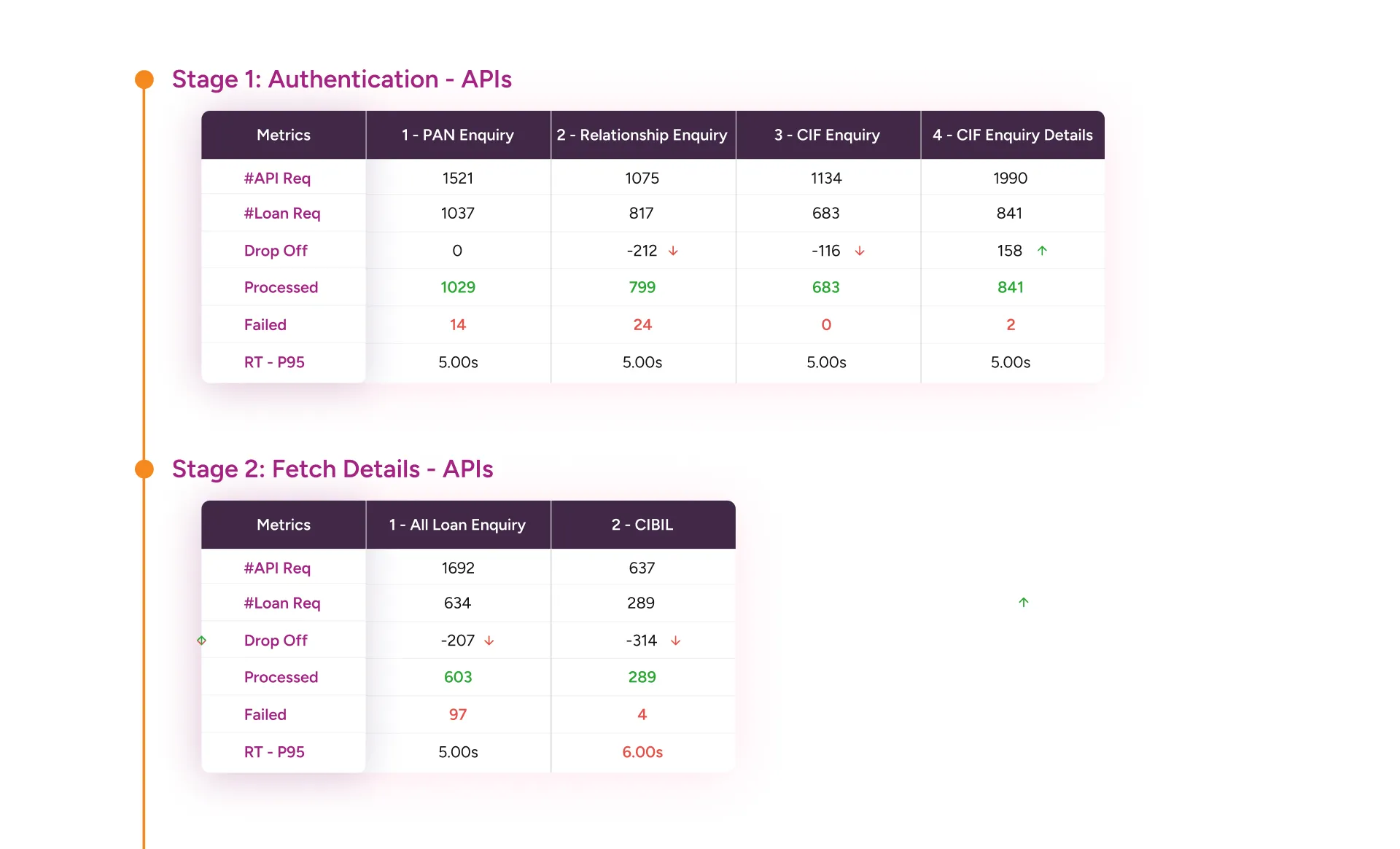

- Correlate Business and Technical Metrics Map business KPIs (e.g., application to disbursal conversion, auto-debit success rate, delinquency rates) to underlying system health

E.g., database latency, API response times, downtime in payment gateways

Fig 3: Business KPIs mapped to system metrics

- Enable Deep Database and Application Observability Identify deadlocks, slow transactions, and query performance issues that impact workflows like fund disbursals, ledger updates or EMI posting.

- Real-time Monitoring of External Touchpoints Whether it's NSDL for PAN validation, CIBIL for bureau scores, or NACH mandate systems - VuNet provides full transparency and alerting for failures, timeouts, and delays.

- Deliver AI-Driven Insights and Anomaly Detection Use machine learning to detect anomalies across business journeys and forecast issues before they escalate. Assist with automated RCA for fastened MTTR.

Examples

- Detect sudden drops in application volumes

- Flag spike anomalies in EMI failures

- Forecast upcoming disbursal or repayment load based on historic patterns.

- Generate Real-Time, Contextual Alerts Receive alerts that aren't just about server spikes, but about business-impacting incidents like failed loan applications or delayed fund transfers.

- Compliance and Audit Readiness Every transaction, every deviation, and every RCA is traceable—critical for regulatory and audit compliance in NBFC operations.

Fig 4: Sample Dashboard for Observability of NBFC Digital Transactions

The Benefits for NBFCs

NBFCs leveraging VuNet’s Business Observability Platform realize tangible outcomes: Faster Incident Resolution: Up to 50% reduction in Mean Time to Detect (MTTD) and Mean Time to Repair (MTTR), especially for loan processing and repayment failures. Higher Customer Satisfaction: 25% improvement in Net Promoter Scores (NPS) by preventing drop-offs in journeys like eKYC, eMandate, or disbursal. Reduced Revenue Leakage: Early detection of failed EMI collections, delayed disbursals, and API breakdowns reduces business impact. Operational Efficiency Gains: Automated RCA across the LOS / LMS / CRM ecosystem frees up operations and engineering teams for strategic initiatives. Better Regulatory Compliance: Full traceability across every lending and servicing touchpoint ensures readiness for audits and inspections. Stronger Business Resilience: Real-time insights allow faster adaptation to traffic spikes, partner failures, or infrastructure issues.

How NBFCs Should Prepare for the Shift

Adopting business observability isn't just a technology upgrade—it requires a mindset and process shift. Here's what NBFCs should do:

- Prioritize Journey Monitoring: Focus on end-to-end observability for key journeys that drive business outcomes like customer onboarding, loan servicing, and repayment collection.

- Enable Event Emission: Enable applications to emit meaningful business events with timestamped, structured logs and metrics at critical junctures such as onboarding and loan application stages, to help track delays and customer pain points.

- Integrate Silos: Break down data silos across infrastructure, application, and business layers.

- Invest in Unified Platforms: Choose solutions like VuNet that are natively designed for NBFC workflows and KPIs.

- Train Teams for New Workflows: Develop operational playbooks focused on business KPIs, not just server uptimes.

Conclusion: Building the Future of Resilient, Responsive NBFCs

The digital future of NBFCs hinges on how well they can see, understand, and act across their business journeys in real time. With VuNet’s Business Observability Platform, NBFCs can finally move from firefighting outages to engineering experiences, ensuring faster disbursals, smoother repayments, and happier customers. The question isn’t whether to adopt business observability—it’s how quickly you can build a real-time, business-aware NBFC ready for tomorrow.